Public Serial Compounders and The Model Behind Long-Term Value

Serial compounders have become some of the most fascinating businesses to study in modern markets. Over long periods of time, many of them have created substantial value by repeatedly acquiring and holding durable businesses rather than relying on short-term growth or large one-off transactions.

At SureSwift Capital, we’ve spent time studying these businesses closely. Over the years, we’ve partnered with and acquired many strong SaaS businesses. As market conditions have become more volatile, we’ve become increasingly interested in how long term acquirers allocate capital and build value across cycles.

In particular, we’ve been looking at public serial acquirers to better understand how they build portfolios, invest capital, and sustain performance over long periods of time. In this post, we break down how these serial compounders operate in practice and which parts of their playbooks are most relevant in a private market context.

Table of Contents:

- What Is a Public Serial Compounder?

- Inside the Serial Compounder Playbook

- How These Companies Perform in Public Markets

- Key Lessons From Leading Compounders

- How This Shapes SureSwift’s Approach

- What Comes Next

What Is a Public Serial Compounder?

Public serial compounders are publicly traded companies that generate long term growth by repeatedly acquiring and holding businesses over many years. Instead of relying primarily on organic growth or a few large transactions, acquisitions become a core and ongoing part of how the business grows.

What sets a serial compounder apart is not just how often they acquire businesses, but how those acquisitions are financed, integrated, and managed over time. These companies typically use internally generated cash flow to fund deals, focus on acquiring durable and self sustaining businesses, and hold them indefinitely rather than optimizing for resale. As a result, capital allocation becomes one of the most important decisions management makes. It determines how much cash is reinvested into the business, returned to shareholders, or used for future acquisitions.

While these models differ from SureSwift in structure and scale, they’re still highly relevant. They illustrate what disciplined capital allocation looks like when acquisitions become a repeatable system rather than a one off event. The consistent focus on cash flow durability, downside protection, and long term value creation closely mirrors how we evaluate opportunities in private markets.

Inside the Serial Compounder Playbook

Market Focus

The strongest public serial compounders are highly intentional about where they operate and what they own. Instead of spreading across many industries, they focus on narrowly defined markets that are fragmented, defensible, and structurally durable. These markets often share characteristics such as mission-critical products or services, high switching costs, regulatory or technical barriers, and long customer relationships.

This focus helps compounders build portfolios where individual businesses behave predictably. Over time, management develops a clear understanding of what “good” looks like within a niche. That includes acceptable margins, reinvestment needs, customer concentration, and downside risk. As that knowledge builds, underwriting tends to improve and the risk of surprises decreases as the portfolio grows.

Structurally, these platforms are typically organized around decentralized operations with centralized capital allocation. Operating companies retain control over pricing, staffing, and customer relationships, while the parent company focuses on setting return thresholds, allocating capital, and pacing acquisitions. This separation allows the portfolio to grow without forcing uniform operating playbooks across very different businesses, while still maintaining financial discipline at the top.

Deal Processing

What differentiates leading serial compounders is not how aggressively they source deals, but how consistently they evaluate them. Acquisitions are treated as an ongoing part of the business rather than occasional events. That means having standardized screening, repeatable diligence processes, and clearly defined investment criteria.

Underwriting is usually centred on cash flow rather than revenue growth. Businesses are evaluated based on earnings durability, customer retention, pricing power, and how stable margins remain through different economic cycles. Growth is valued when it is repeatable and sustainable, but not if it introduces unnecessary risk. In many cases, modest growth combined with high predictability is preferred to faster but less reliable expansion.

Downside protection is just as important. Strong compounders structure acquisitions so that underperformance does not impair the broader portfolio. This often includes conservative leverage, earnouts, or other contingent payments, along with a preference for businesses that can remain cash generative even under stressed conditions. The goal is not to eliminate risk, but to ensure that mistakes are survivable and don’t disrupt the compounding engine.

Financial Discipline

Capital allocation sits at the core of how serial compounder operate. Free cash flow generated across the portfolio is continuously reinvested, creating a cycle where strong operating performance expands the company’s ability to acquire more businesses. Decisions around reinvestment, leverage, and shareholder returns are viewed through the lens of long term compounding rather than short term optimization.

The strongest compounders are also deliberate about payout policies. Dividends and buybacks are not used to maximize near term yield, but to return capital only when internal reinvestment opportunities no longer meet required returns. As a result, payout ratios often fluctuate over time, reflecting the availability of attractive acquisitions rather than a commitment to smooth distributions.

Leverage is used selectively. While some compounders do employ meaningful debt, it is typically supported by stable cash flows and structured in a way that preserve flexibility across cycles. Maintaining the ability to continue acquiring during downturns is often viewed as more important than maximizing returns in favourable conditions.

Operational Structure

Operationally, public serial compounders tend to avoid heavy integration or centralized control. Acquired businesses are expected to continue operating largely independently, with minimal disruption to customers or employees. The parent organization focuses on governance, financial reporting, and performance monitoring rather than day to day management.

Because intervention after acquisition is limited, the quality of the business at entry is critical. Strong management teams, entrenched customer relationships, and proven operating models are prioritized over opportunities that require significant turnaround work. In practice, this means that much of the value creation comes from disciplined buying and steady cash generation rather than aggressive operational change.

Over time, this approach allows compounders to manage large portfolios without overwhelming central resources. It also reinforces the importance of saying no to deals that don’t meet standards, since there is limited capacity to “fix” businesses after they are acquired.

How These Companies Perform in Public Markets

To better understand how public serial compounders behave in the market, we looked at several well known examples and their share price performance over the past year.

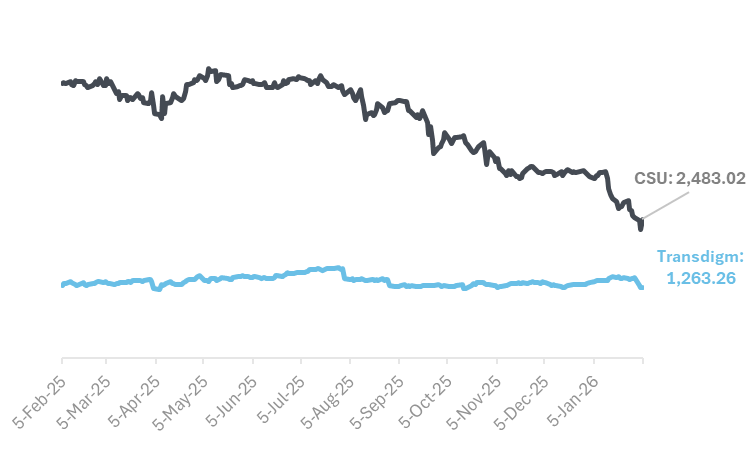

Constellation Software has seen significant swings in its share price over the past 12 months. As of early February 2026, the stock trades around CA$2,430, down roughly 50% from its 52-week highs near CA$5,300. Over that same period the one year return sits around -50%, even as revenue and earnings have continued to grow. Much of the decline appears tied to broader tech sector rotation, incremental earnings misses relative to expectations, and shifts in investor sentiment toward higher growth software stocks. The company currently pays a small quarterly dividend of roughly CA$1.00 per share, representing a yield of about 0.2–0.3%.

Constellation Software vs TransDigm (1-Year Performance)

Exchange Income Corporation trades with a forward dividend yield of roughly 2.8%, supported by monthly dividend payments of about CA$0.23 per share. Its share price tends to move around earnings releases, acquisition announcements across its aviation and services businesses, and changes in analyst coverage. Recent analyst updates in early 2026 pushed price targets higher after stronger earnings results, although payout ratios remain elevated relative to earnings.

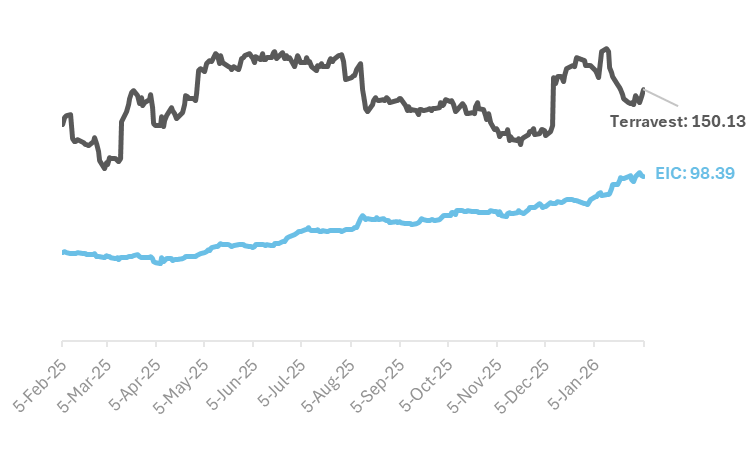

TerraVest Industries currently trades in the CA$150–160 range and pays a quarterly dividend of CA$0.20, representing a yield of roughly 0.5%. Its share price has generally moved alongside dividend growth and steady acquisition driven revenue expansion.

TerraVest Industries vs Exchange Income Corporation (1-Year Performance)

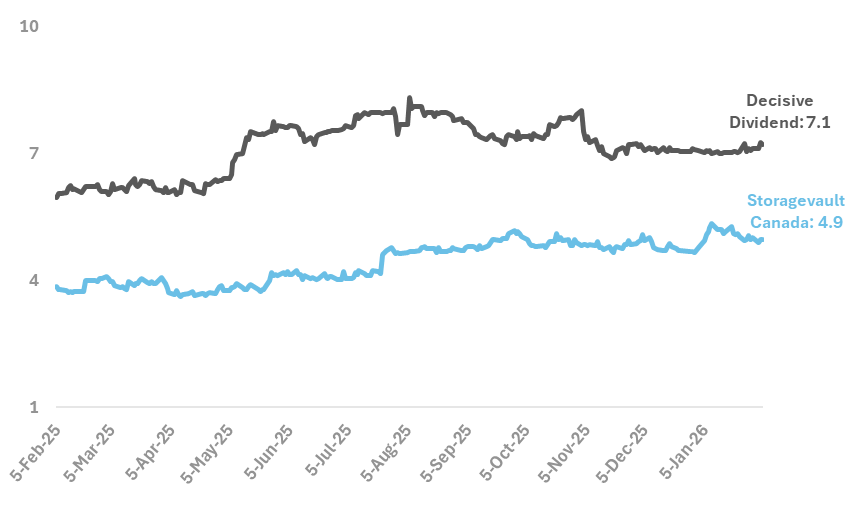

Smaller cap compounders show similar patterns. Decisive Dividend Corporation trades around CA$7–8, with a dividend yield of roughly 7.4%, paid monthly at about CA$0.045 per share.

StorageVault Canada trades around CA$4–5 per share. Its stock performance tends to move with quarterly earnings results, acquisition activity, and updates related to site densification and refinancing.

Decisive Dividend vs StorageVault Canada (1-Year Performance)

Across these companies, share price movements tend to be driven by concrete events such as earnings results relative to expectations, dividend announcements, or changes in analyst coverage. Broader factors like sector rotation and shifts in investor sentiment can also influence performance. While prices may fluctuate, revenue growth, dividend policy, and earnings coverage remain the core signals markets respond to over time.

Key Lessons From Leading Compounders

Cash flow matters more than growth optics

Across the public compounders we studied, acquisition decisions start with cash flow durability rather than revenue growth or market narratives. Businesses are evaluated based on how predictable their earnings are, how they perform through economic cycles, and how much cash they can reliably generate after maintenance costs. This helps explain why many of these companies are willing to accept slower headline growth in exchange for stability, and why valuation discipline often holds even when market conditions are favourable.

Capital allocation drives long term performance

As portfolios scale, capital allocation becomes the main driver of outcomes. Free cash flow is continuously reinvested, and decisions around reinvestment, leverage, and shareholder returns shape long term performance. Dividend policies vary widely across compounders, but in most cases they reflect the availability of internal opportunities rather than an attempt to maximize short term payouts. The consistency of this decision making process matters far more than the specific form capital returns take.

The best deals come from long term relationships

Many successful compounders rely less on competitive auctions and more on long term relationship building. Deals often come from years of dialogue with founders, operators, and intermediaries rather than one off sale processes. This relationship driven approach improves access to proprietary opportunities and creates alignment well before a transaction ever takes place.

Experience compounds in adjacent markets

Rather than constantly moving into unrelated verticals, compounders often stay within adjacent or horizontal markets where experience compounds. Acquiring similar businesses allows teams to transfer operational knowledge, refine their playbooks, and improve underwriting over time. The result is not just portfolio growth, but steadily improving decision making with each acquisition.

How This Shapes SureSwift’s Approach

Studying public serial compounders has helped clarify which principles matter most when acquisitions become a repeatable activity rather than a one time event. Across different sectors and structures, the common thread is discipline around what gets acquired, how capital is invested, and how complexity is managed over time.

For SureSwift, these observations help sharpen what we focus on when evaluating opportunities. Across many of the public compounders we studied, long term outcomes are shaped less by ambitious post acquisition plans and more by how consistently a business generates and sustains cash over time. That perspective reinforces the importance of understanding how a business actually operates, how it performs through cycles, and how capital decisions influence results over long horizons.

These observations also reinforce the value of staying focused within adjacent markets. Familiarity with customer behaviour, cost structures, and operating risks allows for more consistent decision making and clearer expectations at the time of acquisition. Rather than pursuing breadth for its own sake, the approach prioritizes clarity, repeatability, and long term consistency in how businesses are evaluated and supported.

What Comes Next

At SureSwift, we’re applying many of these lessons as we continue refining our acquisition strategy. That means building a repeatable acquisition playbook, leaning into relationship driven sourcing, and staying focused on durable, cash generating businesses where operational improvements can compound over time.

As we continue this work, we’ll keep sharing what we’re learning from research, from operators, and from the businesses we partner with.

If you’re interested in learning more about serial acquirers, or if you’re a founder, broker, or advisor working with an interesting business, we’re always open to connecting and exchanging perspectives. Visit our website to learn more about our investment approach or reach out if you’d like to start a conversation.

.png)

Related articles

.jpg)

Conversion rate optimization for SaaS: What actually works in 2026 (and beyond)

SaaS conversion rate optimization has moved beyond button tests and landing page tweaks. Here’s how modern teams can improve acquisition, activation, and retention by focusing on user intent, faster time-to-value, and smarter full-funnel decisions.

How SaaS Teams Use AI to Improve Email Personalization

The best email personalization strategies don't rely on AI alone. Learn how software businesses are combining AI, customer data, and thoughtful workflows to create more relevant communication at scale, with examples from MeetEdgar and Mailparser.